EBITDA

EBITDA

EBITDA

EBITDA = Net Profit + Interest +Taxes + Depreciation + Amortization, as a % of Income from Operations.

EBITDA is used to analyze a company's operating profitability before non-operating costs (interest, taxes, and other non-core or over/under stated expenses), and non-cash charges (depreciation and amortization).

The EBIT gives a demonstration of the earnings of the business without the destabilizing effect of debts or surplus cash balance.

EBITDA is used by professional investors to analyze and compare potential profitability between companies and industries, because it eliminates the effects of financing and accounting decisions that legally suppress earnings so as to reduce the tax liability.

This particular indicator of a company's financial performance, together with accurate historical financials, allows one to recast the revenue and earnings and thus obtain a more accurate picture of its true earnings & growth potential in projections for the years to come.

Recasting provides an economic view of the company as though it were run by management dedicated to maximizing profitability.

If your 5-year pro forma is NOT based on a recast history, then you will be understating your valuation. Not good for you, but great for the potential buyer or investor.

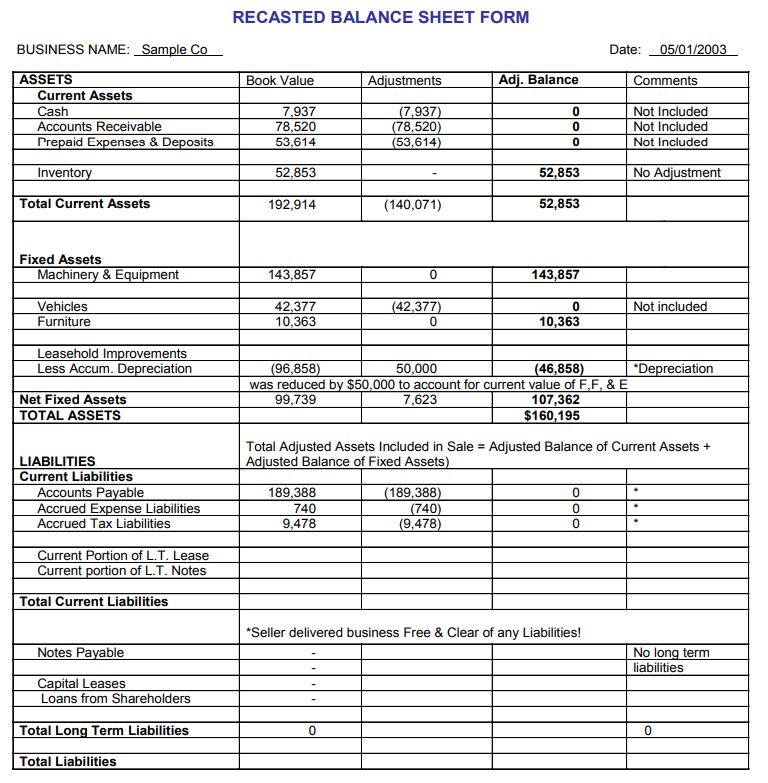

Items that are typically recasted are:

EBITDA does NOT provide an accurate cashflow picture. The DCF-model is used for that.

Operating earnings (EBITDA) and cash earnings are NOT the same thing. Accrual accounting (EBITDA) counts a sale as soon as the product is shipped. Cash accounting counts a sale only when someone paid for it in full.

If products sit in a warehouse before someone actually pays for it, then the company may not have enough cash on hand to pay its creditors and run its daily operations. This could lead to more debt and even bankruptcy.

Thus, the real cash flow is directly affected by the ITDA items. Companies must pay interest and taxes before they can even pay dividends to investors. That cash has to come from somewhere.

The depreciation and amortization items are used to spread the expense of capital investments out over many years. If these capital investments are considerable, ignoring the long-term financial impact of such investments can be very risky.

EBITDA understates the effects that capital structure and CAPEX spending have on a business. It also leaves out the cash required to fund working capital and the replacement of old equipment, which can be significant.

Over-leveraged companies showing only EBITDA are often skirting GAAP (Generally Accepted Accounting Principles) standards and thus fool unsuspecting investors.

Most small businesses are managed to minimize taxable income. Thus, it is often necessary to make adjustments to the reported financial statements in order to express the actual cash flow benefits available for the owner. Due diligence, by adjusting the business financial statements facilitates its comparison to the industry standard ratios.

Here are some more Balance Sheet items that may require adjustment:

Some items on the Profit and Loss Statement that may require adjustment are:

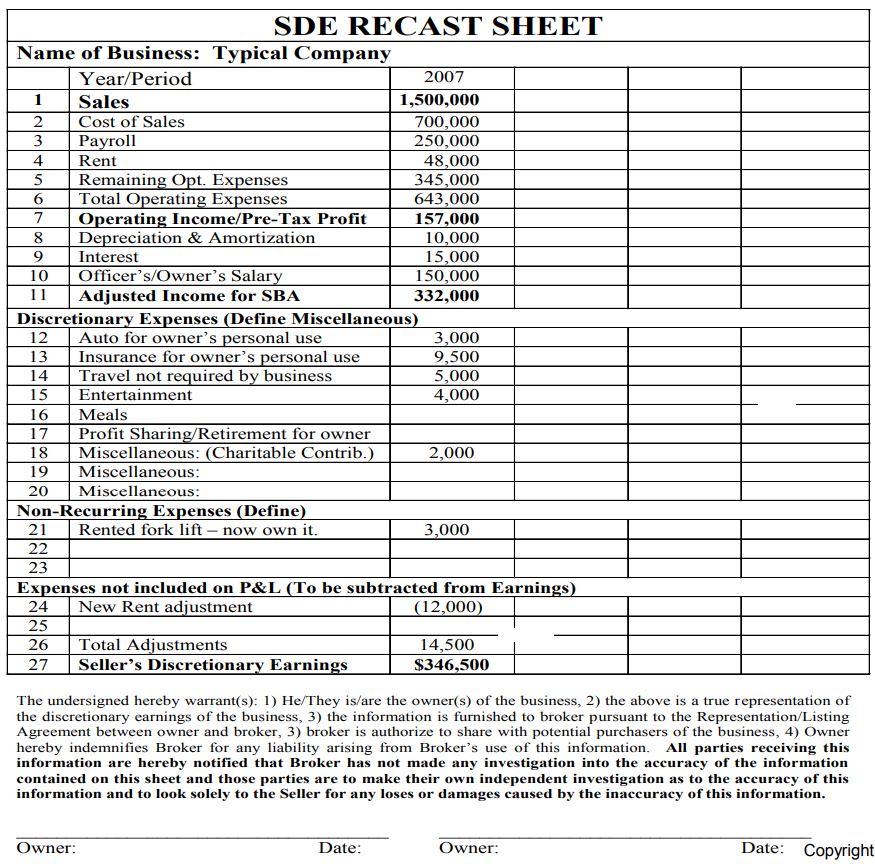

Seller's Discretionary Earnings is measured by EBITDA plus company owners' salaries, compensations and perks: SDE = EBITDA + Owners Compensations. For a more accurate value calculation it is best to use the average SDE over the past 3-5 years.

In business appraisal literature, the process of recasting the financials is also called reconstruction or normalization.

The list below represents key aspects of a business that a smart investor may wish to have examined during the due diligence period, and may serve as a guideline: